The Net Worth Myth:

Why Your “Safe” Business Strategy Is Keeping You Broke

The modern entrepreneur is trapped in a grueling, “sisyphean” cycle. You work harder, you sell more, and you optimize your funnels, yet the feeling of true wealth remains elusive. We have been conditioned by an industrial-age education system to believe that security is paved with “accumulation”—the slow, painful process of scrimping on lattes, maximizing a 401(k), and watching a net worth figure climb like a lethargic mountain.

But for the visionary business owner, this “Old Way” is a sophisticated trap. It prioritizes static snapshots of wealth over the dynamic movement of capital. It tells you to shrink your life to fit a budget when you should be expanding your capacity to produce value. To break free, you must realize that net worth is a myth, diversification is a confession of ignorance, and your greatest asset is not your property, but your Human Life Value (HLV).

Before we can fix your procedures, we must address your philosophy. As the strategist Garrett Gunderson posits, there is a hierarchy to prosperity: the Five Ps.

Philosophy: The root. Contradictions in your basic philosophical premises lead to destruction.

Purpose: Emerging from philosophy, this is your “why.” Only humans can choose a purpose; a dog or a cow cannot.

Psychology: Your philosophical premises shape your psychological experiences.

Procedure: The “how-to.” If you apply new procedures without changing your philosophy, you just get better at staying where you are.

Prosperity: The ultimate outcome when the first four are aligned.

Without an abundance-based philosophy, even the most advanced tax strategy will fail because you will eventually return to a state of scarcity. It is time to shrug off the idea of sacrifice and embrace a model of value creation.

--------------------------------------------------------------------------------

1. Net Worth is a Snapshot; Cash Flow is the Lifeblood

Most people are trained to chase a net worth figure—a simple balance sheet calculation of assets minus liabilities. However, net worth is merely a snapshot in time. It tells you where you have been, not where you are going. It is the “muscle” of your financial body, whereas cash flow is the “blood.” You can survive some muscular atrophy, but if the blood stops flowing, the organism dies.

Consider the “Broke Millionaire.” This is the individual with a $2 million home, fully paid off, and a $2 million IRA. On paper, they are wealthy. In reality, they are often paralyzed by stress. The house doesn’t write checks; the tenant does. If that $2 million home requires property taxes, maintenance, and insurance without producing a dime of income, it is a “lazy asset.” Worse, if the owner’s knowledge of how to manage that wealth hasn’t grown alongside the asset, they possess a massive “Human Life Value liability.”

The 80,000 Bitcoin Lesson

Take the visceral example of an early crypto adopter who mined 80,000 Bitcoin. In the early days, they possessed an asset of astronomical potential value. However, because their financial intelligence and HLV did not match the growth of the asset, they sold it all before it even hit one dollar. They had the property value, but they lacked the mental capital to be a steward of that wealth. When your assets grow faster than your knowledge, you don’t feel wealthy; you feel fear. You fear lawsuits, you fear market crashes, and you fear losing what you don’t understand how to replace.

To move from a “stagnant lake” to a “flowing river,” you must understand the difference between the Great Salt Lake and the Amazon River. The Great Salt Lake is a dead, stinky body of water because it has no flow; it only accumulates. Nobody wants to live there. The Amazon, conversely, is so powerful it pushes fresh water miles into the ocean. It is lush and teeming with life because it is constantly moving.

The Passive Income Index

To evaluate if your assets are “Amazonian” or “Stagnant,” use the Passive Income Index. Rank every investment on a scale of 0 to 5 across five categories:

Immediacy: Does it provide regular cash flow now, or is it a “someday” bet?

Management: How much personal time does it require? If you have to deal with “Tenants, Toilets, and Turnover” (the Triple T), it’s not passive; it’s a second job.

Sustainability: How long will this cash flow last?

Location Independence: Can you manage this from a laptop in Italy?

Growth Potential: Does the cash flow have the ability to increase over time?

If you don’t Manage, Monitor, and Maintain (the 3 Ms) your assets, you will not keep them.

True financial independence is reached when your recurring revenue from assets exceeds your monthly expenses.

--------------------------------------------------------------------------------

2. The Efficiency Flip: Recovering the “Ignorance Tax”

Before you attempt to sell a single new product, you likely have “hidden” revenue sitting inside your existing business. Most entrepreneurs pay a heavy “Ignorance Tax”—money lost to inefficiency. By becoming efficient, you aren’t “scrimping”; you are optimizing. There are four primary levers to recover this cash.

I. Taxes: From Historian to Strategist

Most business owners employ “historian” accountants. These professionals record the funeral; they don’t help the patient live. They tell you what you owed last year. You need a tax strategist who understands how to classify income, choose the right corporate structure, and utilize cost segregation. For many business owners, this single shift can recover $10,000 to $100,000 annually.

II. Interest: The 3 Rs and the 3 Cs

Debt should be viewed through the lens of the 3 Cs: Cash flow, Control, and Collateral. To optimize it, apply the 3 Rs:

Restructure: Refinance high-interest loans into lower-interest environments or bundle them for better terms.

Renegotiate: Use your credit score and loyalty to demand better rates. It is cheaper for a bank to keep you than to acquire a new customer.

Reallocate: This is the most counter-intuitive. If you have $100,000 in a savings account earning 3% and a loan costing you 6%, paying off that loan is a “100% return of savings.” You are buying back your own cash flow.

III. Investment Fees: The Parasite of Algorithmic Compounding

Hidden fees are the silent killers of wealth. Consider 100,000 earning 10% over 30 years. That grows to **1,744,940**. Now, take that same 100,000 but subtract just 0.8% in hidden fees (12B-1 marketing fees, custodial fees, etc.), leaving you with a 9.2% return. Over 30 years, you end up with **1,440,000**. That “small” 0.8% fee cost you over $300,000 because of the loss of algorithmic compounding.

IV. Insurance: Designing for Efficiency

Your insurance agent is often an inadvertent thief, stealing your liquidity through bloated premiums. Design for efficiency: bundle your policies, and raise your deductibles to the highest level you can comfortably pay out-of-pocket.

This lowers your premiums and increases your monthly cash flow, allowing you to redirect those dollars into productive assets.

--------------------------------------------------------------------------------

3. Why “Productive Expenses” Are Your Biggest Growth Levers

The industrial age taught us that all expenses are “bad.” For an entrepreneur, this is a fatal misunderstanding. There is a fundamental difference between a destructive expense (waste) and a productive expense (an investment in HLV).

When you are “too cheap” to hire a specialist, you become the bottleneck of your own company.

If hiring a specialist costs you $5,000 a month but frees up 20 hours of your time—time you can use to generate $20,000 in new business—that “expense” is actually a $15,000 profit center.

The Life-Long Tuition

Garrett Gunderson notes that in his early 20s, he invested $7,500 in Strategic Coach and nearly $2,000 in Landmark Education. At the time, that felt like an enormous expense. However, those programs taught him to identify his “Top 20” relationships and how to speak vision into existence. That $10,000 investment led to millions in revenue.

Similarly, the licensing program for the What Would the Rockefellers Do? book was born from an “expense.” Gunderson spent tens of thousands on writing courses and high-level editors like Tucker Max and AJ Harper. This lowered his net worth initially, but it turned a $10 book into a B2B licensing engine where agencies pay $35,000 to leverage the brand.

“It’s about being willing to suffer for what you love. When we discover what we are willing to pay a price for, we discover our life’s mission and purpose.”

--------------------------------------------------------------------------------

4. The Death of Diversification: Play Inside Your Strike Zone

“Don’t put all your eggs in one basket” is a confession that you don’t know which basket is the best. Diversification is for speculators; focus is for investors.

The master investor Warren Buffett is often cited as a fan of diversification, but in reality, he is a master of Investor DNA. He doesn’t buy mutual funds; he makes acquisitions. When he buys a company, he brings in the “Buffett Way”—ruthlessly cutting inefficiency to drive output. He famously said “no” to the tech boom of the 90s because he didn’t understand the fundamentals. He stayed in his “strike zone.”

The Ted Williams Analogy

Baseball legend Ted Williams batted over .400 because he divided the strike zone into 77 cells. He only swung at pitches in his “happy zone” where he knew he could hit .400. If a pitch was a strike but in a cell where he only hit .230, he let it go. Most entrepreneurs swing at everything because they are afraid of “missing out.”

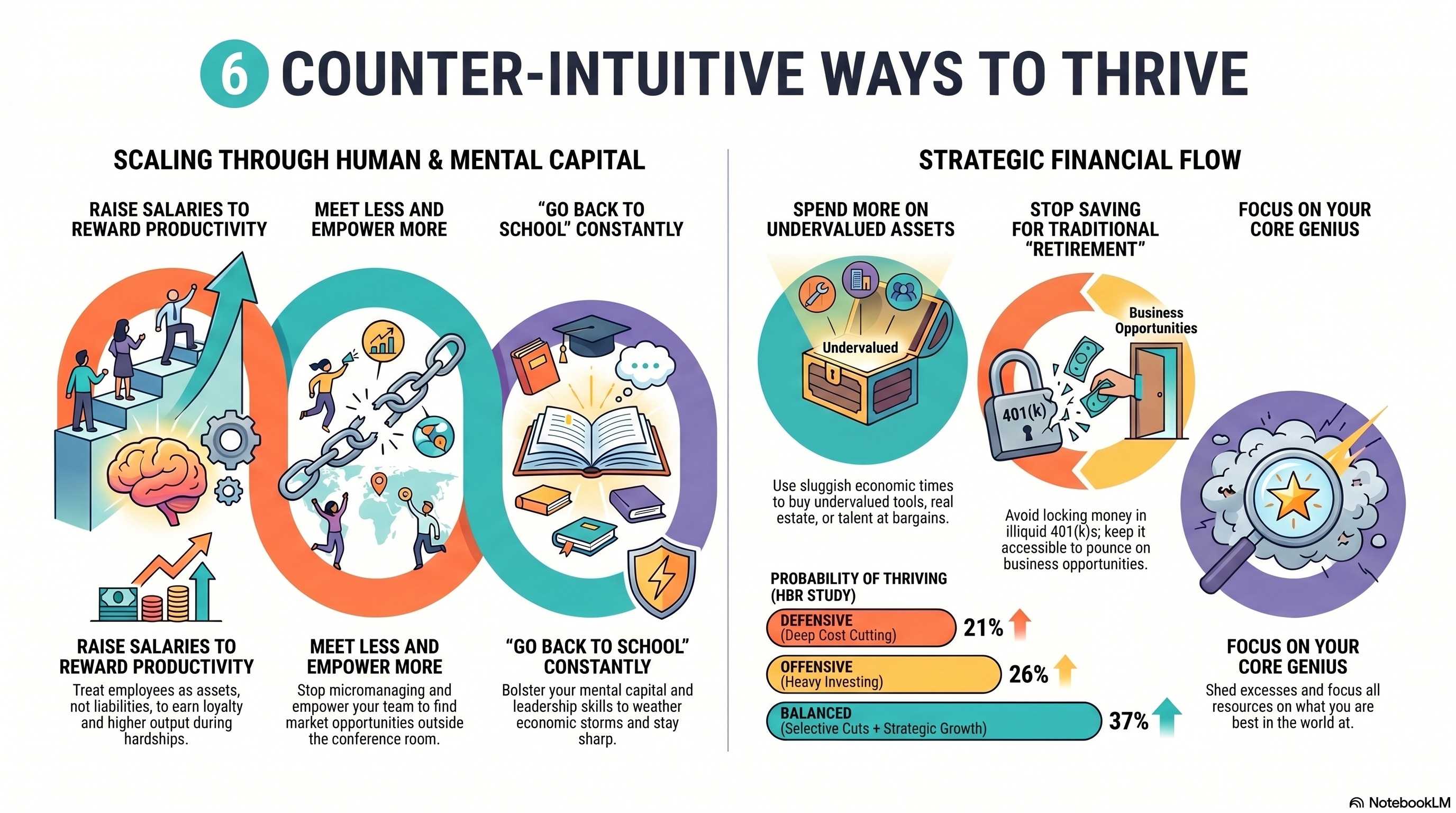

Six Counter-Intuitive Ways to Thrive:

Raise Salaries: Treat employees as assets. Reward them for productivity and they will reward you with loyalty.

Spend More: Buy undervalued assets and tools when others are fearful.

Meet Less: Stop being a “helicopter parent” to your business. Empower your team.

Stop Saving for “Retirement”: Don’t lock money in a 401(k) you can’t touch. Keep it liquid to “pounce” on opportunities.

Focus on the Core: Shed excesses and do what you are best in the world at.

Go Back to School: Constantly bolster your leadership and mental capital.

--------------------------------------------------------------------------------

5. The Rockefeller Method: Legacies Built on Values

The disparity between the Vanderbilt and Rockefeller families is the ultimate cautionary tale of wealth. Cornelius Vanderbilt was the richest man in America, yet within 48 years of his death, a direct descendant died broke. His heirs built ten palaces in Manhattan; today, not one remains. They were “trust fund babies” who knew how to spend, but not how to produce.

In contrast, the Rockefeller fortune is currently empowering its sixth generation. They didn’t just leave money; they left a “perpetual opportunity machine.”

The Francisco d’Anconia Standard

The philosophical heart of the Rockefeller method is captured in this line from Ayn Rand’s Atlas Shrugged:

“Only the man who does not need it, is fit to inherit wealth – the man who would make his own fortune no matter where he started. If an heir is equal to his money, it serves him; if not, it destroys him.”

The Mechanism of Legacy

The Rockefeller Method utilizes a Family Trust and a Statement of Purpose. It acts as a “magnifying glass” for good and a deterrent for evil.

The Family Office: A centralized group of professionals managing the wealth (traditionally requiring a $50M threshold, though now democratized through networks like the Accredited Network).

Yearn to Earn: Heirs do not receive “ends” (cash to buy Ferraris). They receive “means” (loans to start a business, tuition for education, or help with medical disasters).

Conditions for Distribution: Heirs might be required to submit business plans or even book reports (like on Atlas Shrugged) before receiving a dime. This ensures they are “equal to their money.”

--------------------------------------------------------------------------------

6. Shifting from 10% Savings to 100% Velocity

Traditional financial planning—the “10% for 30 years” model—is a slow-death strategy. It relies on the “hope and pray” method. The Enlightened Wealth Strategist focuses on Velocity.

The Nik Halik Case Study

Nik Halik is the ultimate example of “Making It Count.” As an 8-year-old boy in Australia with severe asthma, he wrote a “screenplay” of 10 goals, including becoming a rockstar, an astronaut, and eating lunch on the Titanic. Most would call these impossible.

Nik reached economic independence in his 20s not by being a millionaire, but by ensuring his investment income covered his expenses twice over. He followed a strict protocol:

9 Months of Liquidity: Before investing, he built a foundation of cash.

Avoided Diversification: He became an expert in one area at a time.

Recession Pouncing: He kept money liquid so that when the economy bled, he could buy assets at a discount.

Nik eventually ate lunch on the bow of the Titanic and became a backup astronaut for the International Space Station. He even has a plan for goal #10: his cremated remains will be sent to the moon.

The 10x Advantage

Once you reach a 2:1 ratio (where assets produce twice what you spend), you hit a “10x advantage.” Since your assets cover your lifestyle, 100% of your active income from your business can be poured back into building more assets. This creates a geometric explosion of wealth that accumulation-based models can never match.

--------------------------------------------------------------------------------

7. The Idea Optimizer: Momentum Over Perfection

Business is a game of imperfection. Most entrepreneurs fail because they spend too much capital on an unproven “vision.” To stay profitable from Day One, use the Idea Optimizer.

The Value Equation

Mental Capital x Relationship Capital = Financial Capital. Money is not the starting point. Ideas and networks are.

The Cycle of Creation

Concept to Concrete: Define exactly what the value is, what the liabilities are, and what resources you have to bridge the gap.

The Beta/Pre-selling Strategy: Before you build a “healing center” or a “book condensing service,” sell it. If people won’t write a check for the concept, they won’t write one for the reality.

Co-creation vs. Collaboration: Co-creation with one person creates momentum. Collaboration with many creates exponential growth.

Take the example of an entrepreneur wanting an “off-the-grid healing center.” Instead of buying land and building a restaurant immediately, the “Idea Optimizer” suggests starting with a referral network of existing healers. Host a one-day “spa event” to test the market. Only once the cash flow is proven do you bring the assets in-house.

-------------------------------------------------------------------------------

Conclusion: Your 3-Point Action Roadmap

The Industrial Age taught us to retire from our businesses—to escape a life of drudgery. The Master Synthesizer retires in their business. You delegate the tasks you hate (the “drudgery”) and focus exclusively on the parts of the business that provide joy and create the most value.

Are you ready to retire in your business, or are you still waiting for a “someday” that will never come? To begin your transition today, follow this roadmap:

Immediate Cash Recovery: Identify one “Financial Leak.” Call a tax strategist or renegotiate a high-interest loan. Recover that “Ignorance Tax” within the next 48 hours.

Invest in HLV: Identify one skill or mentor (like a Dan Martell or a Strategic Coach) that will free you from being the bottleneck. This is a productive expense—commit to it.

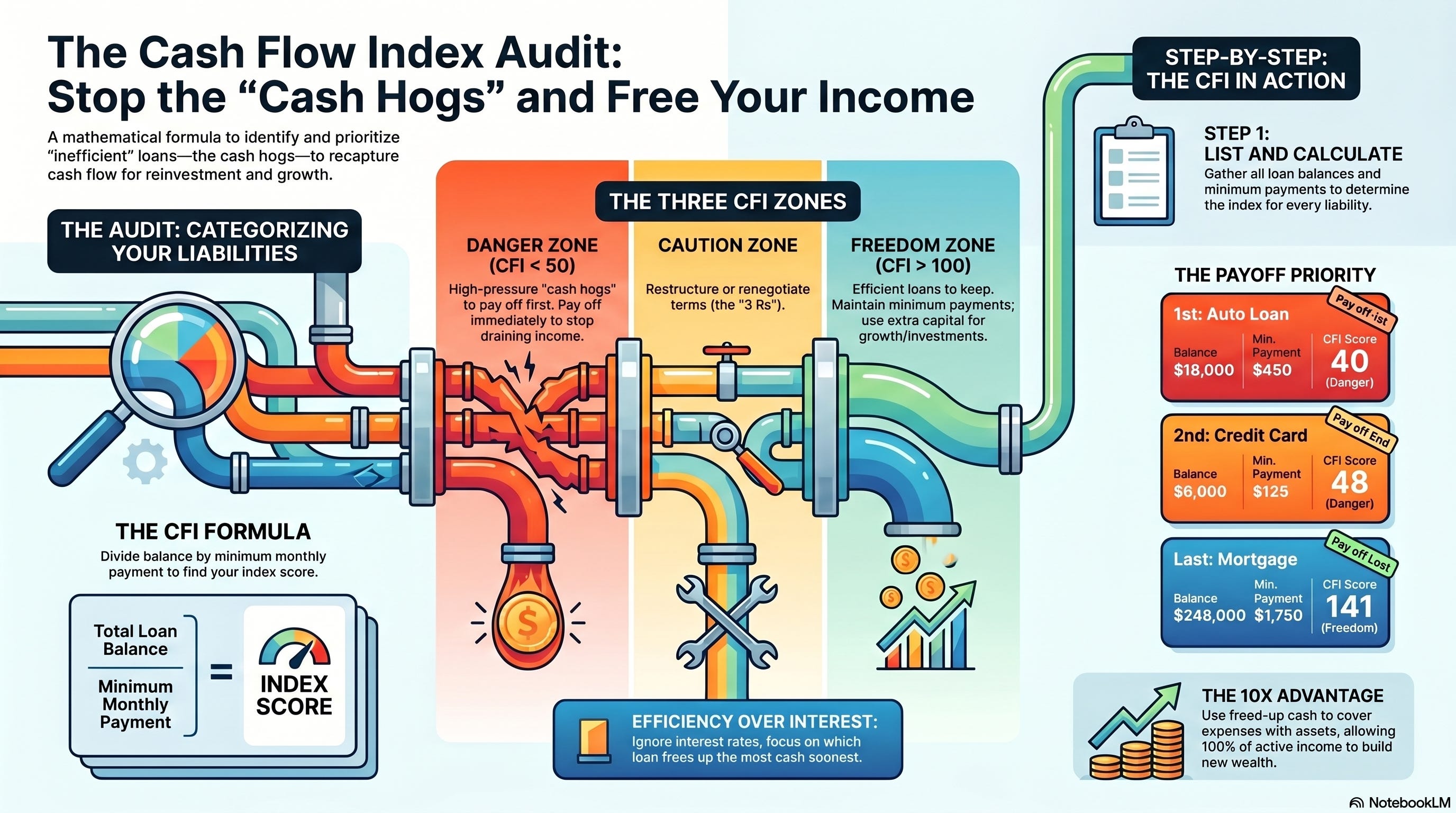

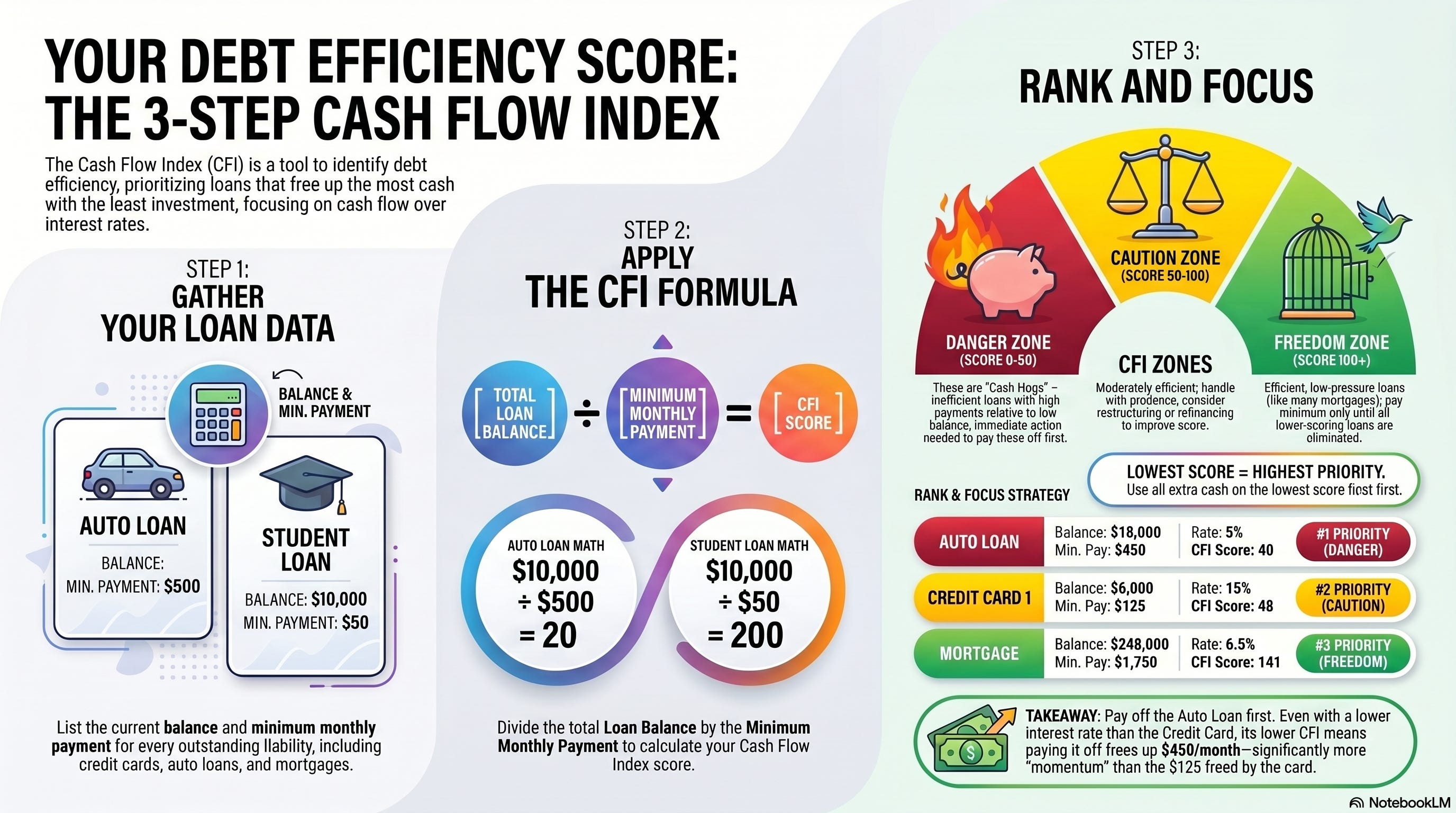

The Cash Flow Index Audit: List your liabilities. Calculate your Cash Flow Index (Balance / Minimum Payment).

CFI < 50: High-interest “clogs.” Pay these off first to free up cash flow.

CFI 50–100: Restructure or renegotiate.

CFI > 100: These are efficient loans. Do not rush to pay them off; use that capital for HLV growth instead.

True wealth is not a static number on a screen. It is the ability to live your Soul Purpose, powered by a legacy of values and a consistent, flowing stream of capital. Stop chasing snapshots and start building your lifeblood.

Disclaimer: The content on this site is for educational purposes only and should not be construed as tax, legal, or financial advice. Although every effort has been made to ensure the accuracy of the information, the author does not assume any liability for any loss or damage caused by errors, omissions, or actions taken by readers. The ideas and strategies shared are the opinions of the author; should you decide to move forward on any financial decision, please consult a qualified professional