The Value Equation:

The Counter-Intuitive Secret That Proves It Doesn’t Take Money to Make Money

1. Introduction: The Great Financial Myth

The most expensive tax you will ever pay is not to the IRS—it is the “ignorance tax” you pay for believing the lies of the financial elite.

The most pervasive lie in the world of finance is the idea that “it takes money to make money.” This is more than a simple error; it is a “liability of ignorance” that creates mental and financial atrophy. It keeps you trapped in a scarcity mindset, waiting for a permission slip from a bank or a 401(k) statement that may never come. Traditional “Accumulation” is a losing game where you’re told to scrimp, save 10%, and hope that after 30 years of market volatility and fees, you’ll have enough to survive.

I’m here to shrug off the idea of sacrifice. True wealth is not about hoarding a pile of cash; it is about Economic Independence—the state where your assets create enough recurring cash flow to cover 100% of your expenses, freeing you to focus on your Soul Purpose.

The Traditional Retirement Path vs. The Financial Independence Path

The Traditional Path (The “Wait and Hope” Model): Reduce your quality of life today, save 10% in a qualified plan you can’t touch until 59.5, and pray the “financial predators” don’t eat your returns in hidden fees.

The Financial Independence Path (The “Producer” Model): Invest in your ability to provide value, create cash-flowing assets today, and cover 100% of your lifestyle so that 100% of your active income can be reinvested.

--------------------------------------------------------------------------------

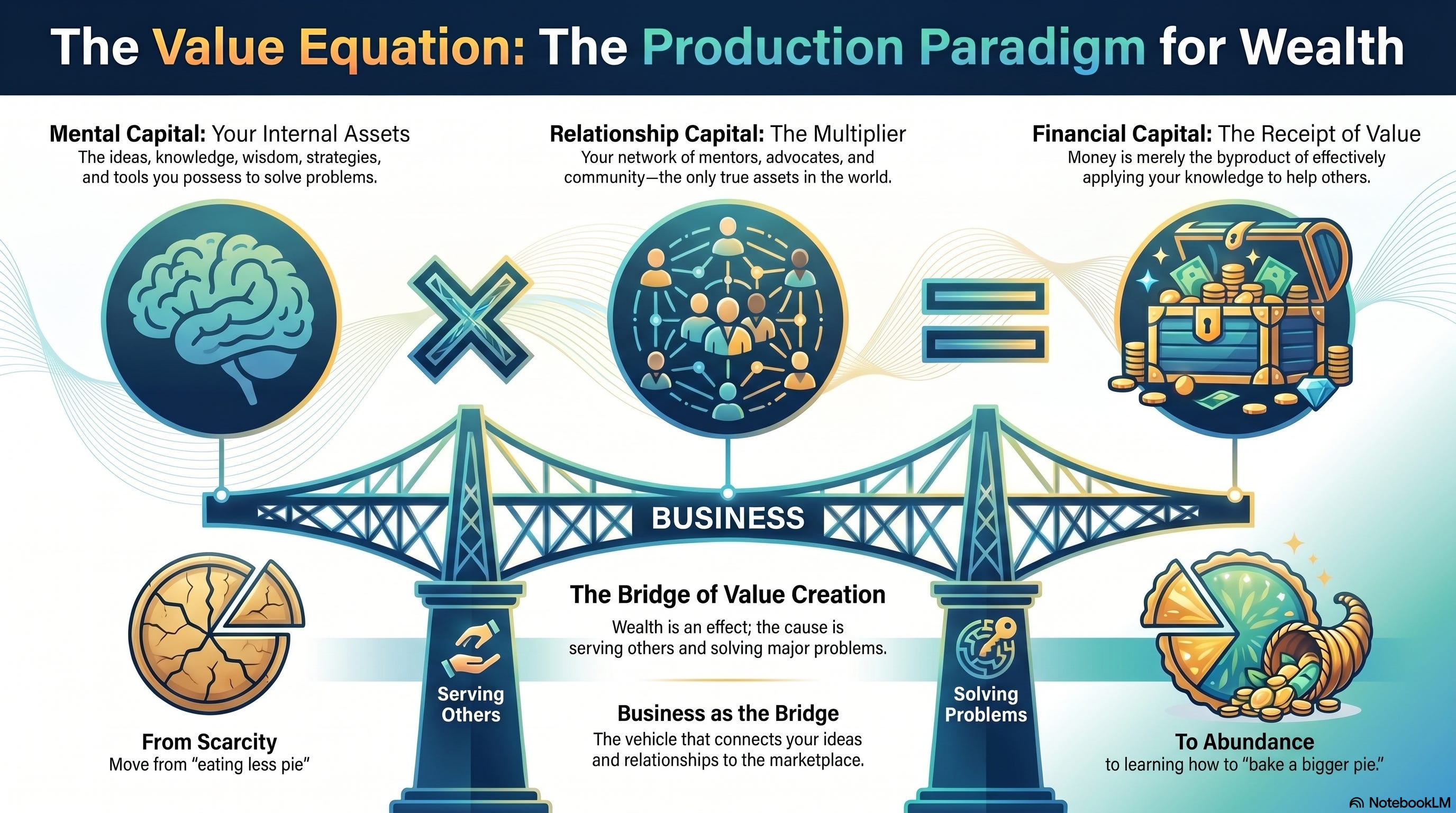

2. The Formula for Wealth: Introducing the Value Equation

Wealth is not a byproduct of luck; it is a mathematical certainty when you apply the right synergy. If you want to stop chasing money and start producing it, you must master the Value Equation:

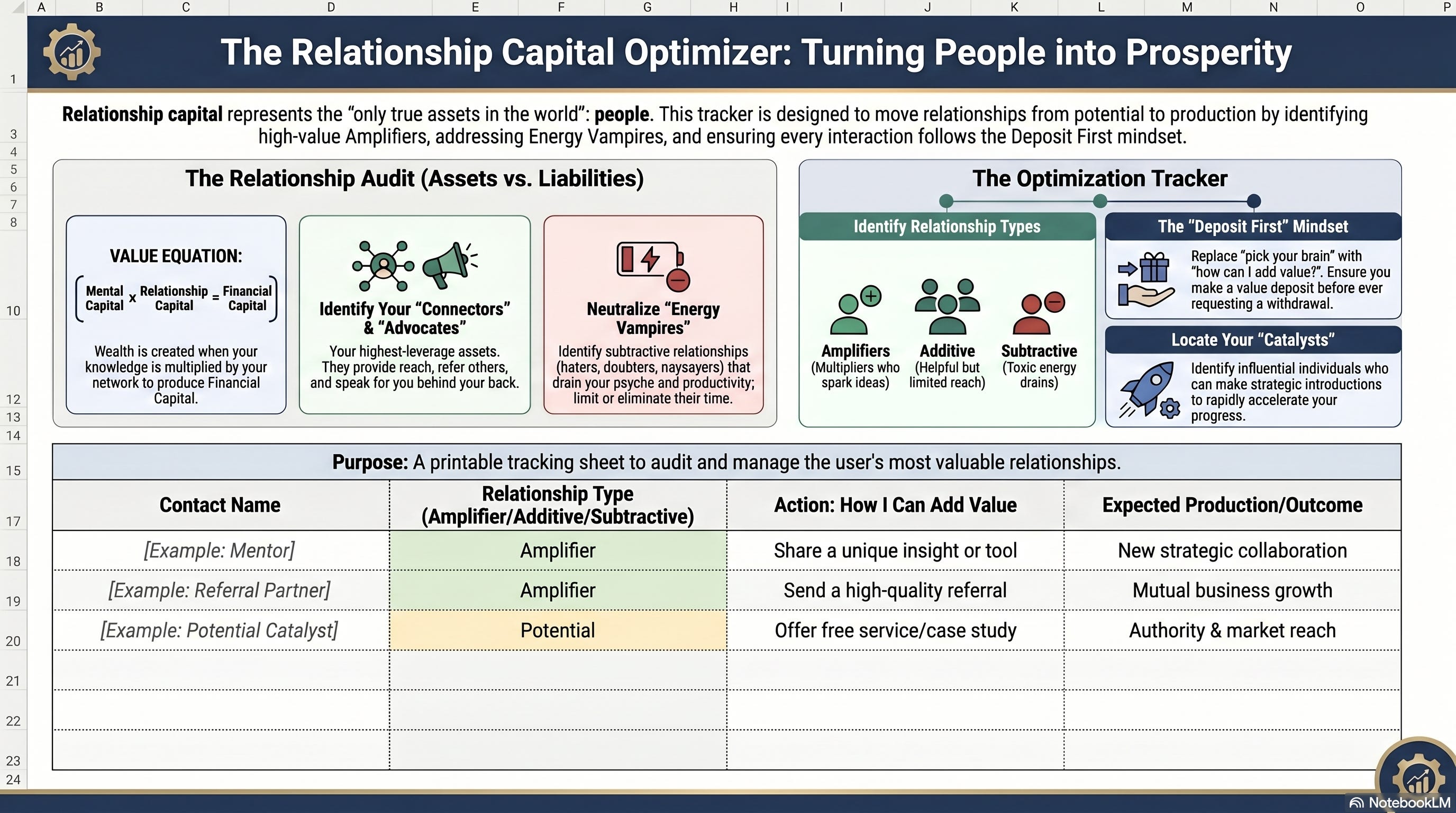

Mental Capital x Relationship Capital = Financial Capital

Mental Capital: This is your “Human Life Value”—your ideas, knowledge, wisdom, skills, and character. This is your primary asset. Property is merely the way we organize human life value to make it useful. If you don’t grow your knowledge as your assets grow, you create a “gap” that leads to fear and loss.

Relationship Capital: These are your networks, your mentors, and your “Top 20” relationships. These are the people who help you achieve your vision faster. Access to experts, like the coaching provided by Dan Sullivan and Babs Smith at Strategic Coach, acts as an accelerator that bridges the gap between your current state and your vision.

Financial Capital: This is the “bloodline” of your finances. It is a byproduct—a flow—that results from the synergy of your mental and relationship capital being deployed to solve problems for others.

--------------------------------------------------------------------------------

3. Human Life Value vs. Property Value

The world tells you to focus on property value: your home equity, your 401(k), your stocks. But property has zero value if it isn’t supporting Human Life Value. In fact, property can become a liability. If you have a $2 million 401(k) but it creates constant stress because of market volatility and tax uncertainty, you have a “Human Life Value liability.” Stress, fear, and lack of control are the ultimate forms of financial atrophy.

Human Life Value Assets:

Intangibles: Skills, Wisdom, Character

Soul Purpose: Unique Authority (Your “Miles Davis”)

Networks: Top 20 Relationships, Mentors

Mindset: Abundance, Resourcefulness, Vision

Property Value Assets:

Tangibles: Real Estate, Business Equity

Paper Assets: Stocks, Bonds, 401(k)s

Liquidity: Cash, Savings, “War Chest”

Physical: Equipment, Inventory, Property

--------------------------------------------------------------------------------

4. Case Study: The Rockefellers vs. The Vanderbilts

The difference between a legacy that lasts and one that disappears in three generations (”shirtsleeves to shirtsleeves”) is the difference between transferring the ends (money) and the means (principles).

Vanderbilt: The Spendthrift Path (The “Ends” Model)

The Fortune: Cornelius Vanderbilt left $100 million in 1877—more than the U.S. Treasury held at the time, or roughly $200 billion today.

The Failure: He left a lump sum with the command to “keep the money together,” but no system to do so. His heirs became socialites, consuming the wealth on Manhattan palaces like The Breakers.

The Result: Within four generations, the fortune was squandered. Direct descendants died broke. They consumed the “ends” without understanding the “means.”

Rockefeller: The Perpetual Opportunity Machine (The “Means” Model)

The Fortune: John D. Rockefeller amassed $1.5 billion (estimated up to $341 billion today) by refining oil for the “poor man.”

The Success: His son, “Junior,” didn’t just hand over cash. He created a Family Office and trusts managed by professionals with a rigorous vetting process.

The System: They focused on a “Statement of Purpose” (the “Why”) and principles of self-sufficiency. Heirs aren’t just given money; they are given opportunity to replicate wealth.

The Result: Six generations later, the fortune is over $10 billion, supporting 150+ heirs and massive philanthropy. They transferred the means to create wealth, not just a sum to consume.

--------------------------------------------------------------------------------

5. Dismantling the Scarcity Trap: Isolation vs. Collaboration

Isolating yourself is the ultimate form of scarcity. Hoarding cash without flow is like the Great Salt Lake—a dead, stinky body of water because it has no outlet. Wealth must function like the Amazon River, lush and life-giving because it is in a constant state of flow.

Velocity is the key to abundance. Money is like blood; you can lose muscle and survive, but if the blood flow stops, you die. Giving more value always leads to receiving more, provided you stay in the flow of collaboration.

The Power of Collaboration When I launched the licensing for What Would the Rockefellers Do?, I could have chased a $25,000 speaking fee. Instead, I flew to Dallas and spoke for a strategic partner for free. I poured into him to build an advocate. That collaboration eventually got my content approved by one of the largest insurance firms in the world, leading to millions in licensing revenue. Collaboration creates exponential growth; isolation creates a dead end.

--------------------------------------------------------------------------------

6. The “Economic Independence” Flip: From 10% to 100%

The traditional model tells you to take 10% of your income and put it into assets you can’t touch. The “Flip” strategy starts with the balance sheet. You invest in your Human Life Value to increase your ability to produce, which allows your assets to eventually cover 100% of your expenses.

This requires choosing the path of Hard/Easy (doing the hard work of building systems and skills now so life is easy later) over Easy/Hard (taking the “easy” route of mindless saving and ending up with a “hard” life of scarcity).

The Three-Step Process to “The Flip”:

Increase Human Life Value: Spend on “Productive Expenses”—mentors, specialized education (like Strategic Coach or Landmark), and hiring talent. This increases your ability to produce value.

Create Cash-Flowing Assets: Shift from “lazy assets” (home equity, stagnant 401ks) to assets that produce recurring revenue (intellectual property, business units, or real estate).

Cover Your Lifestyle: When asset cash flow covers 100% of expenses, you are independent. Now, 100% of your active income can be reinvested, giving you a 10x Advantage over the 10% saver.

--------------------------------------------------------------------------------

7. Actionable Takeaway: Reframe Your Question

Stop asking, “How do I make more money?” and start asking, “How do I reach more people, or more deeply impact the people I already reach?” Money is simply the harvest that follows the planting of value.

The Producer’s Action Plan

Identify your “Miles Davis”: Find your unique authority and “Soul Purpose.” Be willing to be polarizing—if you blend in, you disappear.

Apply the “5 and 5” Rule: Identify 5 things to do more of and 5 things to permanently delegate or eliminate this week to free up mental capital.

Audit Your Efficiency (The 4 Levers): Look for leaks in Tax (overpaying), Interest (the 3 R’s: Restructure, Renegotiate, Reallocate), Investments (hidden fees), and Insurance (improper design).

Eliminate the “Ignorance Tax”: Remember the math: $100k at 10% for 30 years is $1.74M. At 9.2% (due to just 0.8% in hidden fees), it’s only 1.4M. That **300,000 loss** is a direct tax on your ignorance.

Start the Cycle of Creation: Don’t wait for a perfect product. Pre-sell your idea to one “fan” or co-creator today to ensure it is “profitable from day one.”

--------------------------------------------------------------------------------

8. Conclusion: Building a Legacy That Lasts

Money is merely a tool. If an heir is equal to their money, it serves them; if they are not, it destroys them. Simplification and focus equal wealth; complication and distraction destroy it. Invest in your Human Life Value first, as it is the only asset that cannot be confiscated by taxes, lawsuits, or market crashes. Build a system that transfers principles, not just pennies.

Build the Life You Love,

Debi Hawkins

I couldn't agree more with what you're saying here. Traditional financial advice is as flawed as education, healthcare, etc. I look forward to reading more. Thanks!

Thanks Debi. I enjoyed reading this. I especially like the idea of mental capital being your primary asset.